Understanding Condo Loans: Warrantable vs. Non-Warrantable Navigating the world of condo mortgage financing can feel overwhelming, especially…

Strategic Wealth Management: Advanced Reverse Mortgage Strategies for Columbus Retirees

Retirement planning in Columbus, OH has evolved significantly over the last decade. For many seniors, the home is no longer just a place to live—it is their largest financial asset. With property values in Central Ohio seeing steady appreciation, many retirees are sitting on significant equity but may be cash-constrained or worried about outliving their savings.

At Sauk Mortgage Group, we believe in looking at the whole financial picture. While many people view a reverse mortgage solely as a “loan of last resort,” financial planners and savvy homeowners are increasingly using them as a proactive wealth management tool. Whether you are looking to protect your investment portfolio, delay Social Security, or simply age in place comfortably in Franklin County, understanding reverse mortgage strategies can be a game-changer.

In this comprehensive guide, we will explore how a Home Equity Conversion Mortgage (HECM) works, compare it to traditional financing, and outline five specific strategies to enhance your retirement security.

What is a Reverse Mortgage (HECM)?

Before diving into high-level strategies, it is essential to understand the basics. A Home Equity Conversion Mortgage (HECM) is a loan available to homeowners aged 62 and older that allows them to convert part of the equity in their homes into cash. The loan is insured by the Federal Housing Administration (FHA).

Unlike a traditional mortgage where you make monthly payments to a lender, with a reverse mortgage, the lender pays you. You can receive these funds as:

- A lump sum

- Monthly payments (tenure or term)

- A growing line of credit

- A combination of the above

Crucial Requirement: You remain the owner of the home. You must continue to pay property taxes, homeowners insurance, and maintain the property. The loan is typically repaid when the last surviving borrower moves out, sells the home, or passes away.

5 Strategic Uses of Reverse Mortgages for Columbus Homeowners

Joe Sauk, President of Sauk Mortgage Group, has been originating loans since 1993. Over decades of serving the Columbus, OH community, we have seen how strategic equity usage can stabilize retirement. Here are the top strategies we recommend considering.

1. The Standby Line of Credit Strategy

One of the most powerful—and underutilized—features of a HECM is the Standby Line of Credit. Unlike a traditional Home Equity Line of Credit (HELOC), a reverse mortgage line of credit cannot be frozen or cancelled by the lender as long as you meet the loan obligations.

Even more impressive is the growth feature. The unused portion of your line of credit grows at the same compounding rate as the interest rate on the loan. This means your access to borrowing power increases over time, independent of your home’s value.

Strategy: Open the reverse mortgage early in retirement but do not draw on it immediately. Let the line of credit grow. This creates a substantial safety net for future health care costs or long-term care needs.

2. Mitigating “Sequence of Returns” Risk

If you rely on an investment portfolio (like a 401k or IRA) for retirement income, your biggest enemy is a market downturn early in your retirement. If the market drops 20% and you are forced to sell stocks to pay your bills, you lock in those losses and deplete your portfolio rapidly.

Strategy: Use a reverse mortgage line of credit as a buffer asset. When the market is down, stop drawing from your investment portfolio and draw from your home equity instead. When the market recovers, switch back to your portfolio. This allows your investments time to rebound, significantly extending the life of your retirement funds.

3. Eliminating Monthly Mortgage Payments

Many seniors in Columbus still carry a traditional mortgage into retirement. The monthly principal and interest payments can eat up a large chunk of fixed income from Social Security or pensions.

Strategy: Use a reverse mortgage to pay off your existing traditional mortgage. This eliminates the monthly mortgage payment immediately (though you still pay taxes and insurance). This strategy instantly improves monthly cash flow, giving you more breathing room for daily living expenses or leisure.

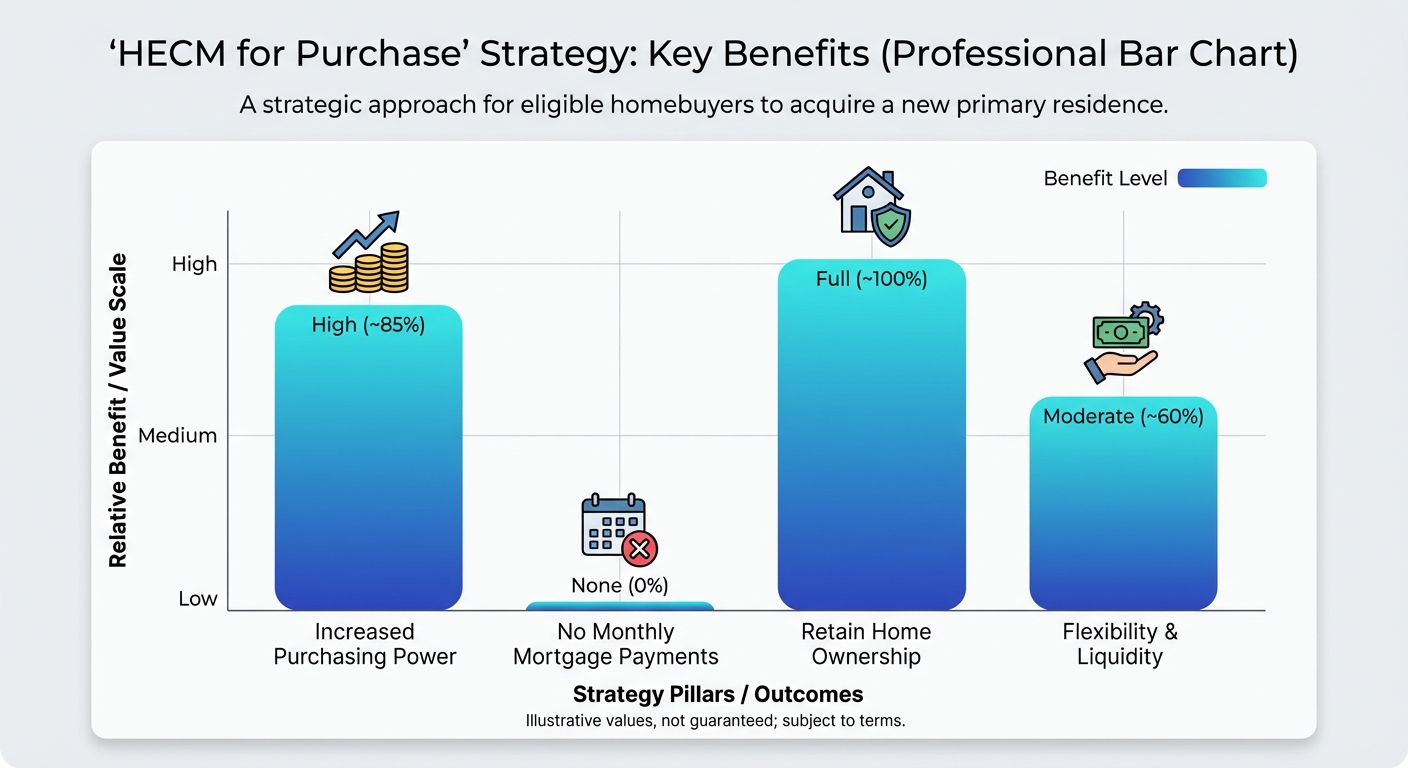

4. The “HECM for Purchase” Strategy

Did you know you can use a reverse mortgage to buy a new home? This is known as the HECM for Purchase program. This is ideal for seniors wanting to downsize, move closer to family in Ohio, or move into a single-story home that is safer for aging.

Strategy: Instead of paying all cash for a new home or taking on a new traditional mortgage, you put down a substantial down payment (using cash from the sale of your previous home) and use the HECM to cover the rest of the purchase price. You move into the new home with no monthly mortgage payments.

For more on purchasing homes, visit our Learning Center.

5. Funding Aging-in-Place Renovations

Most seniors prefer to stay in their own homes as they age. However, multi-story homes in neighborhoods like Clintonville, German Village, or Upper Arlington may require modifications to be safe.

Strategy: Utilize the equity release to fund necessary renovations such as installing stairlifts, widening doorways, upgrading to a walk-in tub, or moving the master bedroom to the first floor. This investment in the property allows you to remain independent in your beloved home for years longer.

Comparison: Traditional HELOC vs. Reverse Mortgage Line of Credit

Many clients ask us at Sauk Mortgage Group why they shouldn’t just get a standard bank HELOC. While HELOCs are great tools, they carry risks for retirees that HECMs do not. The table below outlines the key differences.

| Feature | Traditional HELOC | Reverse Mortgage (HECM) Line of Credit |

|---|---|---|

| Monthly Payments | Required (Interest-only or Principal + Interest) | None Required (Voluntary payments allowed) |

| Credit Line Growth | No. Limit is fixed. | Yes. Unused portion grows over time. |

| Cancellation Risk | Lender can freeze or reduce limit if home value drops or credit score changes. | Guaranteed. Cannot be frozen or reduced as long as loan terms are met. |

| Income Requirements | Strict debt-to-income ratios. | Flexible “residual income” assessment. |

| Repayment Trigger | End of draw period (usually 10 years) triggers full repayment or amortization. | Repayment only when you move, sell, or pass away. |

Why Local Expertise Matters in Columbus, OH

Real estate is inherently local. The housing market in Columbus has unique characteristics compared to the national average. As the “Heart of Ohio’s Innovation Corridor,” our region has seen robust growth. However, navigating the appraisal process and understanding local condo approvals or property requirements requires a local touch.

At Sauk Mortgage Group, we aren’t a faceless call center. We are your neighbors. Joe Sauk and the team understand the nuances of Franklin County property values. Whether your home is a historic property in Victorian Village or a suburban home in Dublin or Westerville, we know how to maximize your appraisal value to ensure you get the most benefit from your equity.

We invite you to meet our team and see why personalized service makes a difference when making decisions about your largest asset.

Addressing Common Misconceptions

- Myth: The bank takes my house.

Fact: You retain the title to your home. The bank simply has a lien on the property, just like a traditional mortgage. - Myth: I can end up owing more than the house is worth.

Fact: HECMs are “non-recourse” loans. This means neither you nor your heirs will ever owe more than the loan balance or 95% of the home’s appraised value at the time of sale, whichever is lower. The FHA insurance covers the difference. - Myth: My children will be burdened with debt.

Fact: Your heirs are not personally liable for the debt. They can choose to sell the home to repay the loan and keep the remaining equity, refinance the home into their own name, or walk away without penalty if there is no equity left.

The Sauk Mortgage Group Advantage

Choosing the right partner for your reverse mortgage is critical. Sauk Mortgage Group is committed to serving our customers with honesty, integrity, and competence. Joe Sauk has been helping borrowers overcome roadblocks and secure loans since 1993.

We offer:

- Personalized Consultations: We sit down with you (and your family or financial advisor) to ensure this is the right move.

- Competitive Rates: Our goal is to provide the lowest interest rates and closing costs available in Ohio and Florida.

- Education First: We prioritize your understanding of the product over making a sale.

If you are considering refinancing or exploring reverse mortgage options, check our Today’s Rates or simply give us a call.

Frequently Asked Questions (FAQs)

1. How much money can I get from a reverse mortgage in Columbus, OH?

The amount you can borrow depends on three main factors: the age of the youngest borrower (or eligible non-borrowing spouse), the current interest rate, and the lesser of the appraised value of your home or the FHA lending limit ($1,149,825 for 2024). Generally, the older you are and the lower the interest rate, the more funds you can access.

2. Is the money I receive from a reverse mortgage taxable?

Generally, no. The IRS typically considers proceeds from a reverse mortgage as loan advances, not income. Therefore, they are usually tax-free. However, we strongly recommend consulting with a tax professional to discuss your specific situation.

3. Can I lose my home with a reverse mortgage?

Foreclosure can only occur if you fail to meet the loan obligations. The primary obligations are: keeping the home as your primary residence, paying property taxes and homeowners insurance on time, and maintaining the property in good condition. As long as you meet these terms, you can live in the home for the rest of your life.

4. What happens if I want to sell my home later?

You can sell your home at any time. When you sell, the reverse mortgage loan balance (principal plus accrued interest) must be paid off. Any remaining equity belongs to you. There are no prepayment penalties for paying off the loan early.

5. Can I get a reverse mortgage if I have bad credit?

Reverse mortgages are generally easier to qualify for than traditional loans because there are no monthly mortgage payments required. However, there is a financial assessment to ensure you have the capacity to pay your property taxes and insurance. If credit is an issue, we may be able to set aside a portion of the loan proceeds (a Life Expectancy Set-Aside) to pay these expenses for you.

Take Control Today

Your home has served you well over the years; now it’s time for it to return the favor. A strategic reverse mortgage can provide the financial freedom to enjoy your retirement in Columbus without the stress of monthly payments or cash flow concerns.

Don’t navigate this complex financial landscape alone. Contact Joe Sauk regarding your options today. We are ready to listen to your story and help you achieve your goals.

Ready to discuss your strategy?

Click Here to Contact Us

Or call us directly at (614) 353-5088

Email: joe@saukmortgagegroup.com

Related Posts