Why Choose a 30-Year Fixed-Rate Mortgage? When it comes to buying a home or refinancing…

The Complete Guide to Condo Mortgage Financing in Columbus, OH

Understanding Condo Loans: Warrantable vs. Non-Warrantable

Navigating the world of condo mortgage financing can feel overwhelming, especially if you are a first-time buyer or looking for an investment property mortgage in the vibrant Columbus, OH market. Unlike single-family homes, securing a condo loan involves not just evaluating your financial profile, but also the financial health and structure of the condominium association itself.

At Sauk Mortgage Group, led by local expert Joe Sauk, we specialize in helping buyers secure the right condo loans. One of the most critical concepts to understand is the difference between warrantable and non-warrantable condos:

- Warrantable Condos: These properties meet the strict guidelines set by Fannie Mae and Freddie Mac. They are generally easier to finance using a conventional fixed-rate mortgage or an FHA purchase loan. Features usually include a high percentage of owner-occupied units and a financially sound homeowners association (HOA).

- Non-Warrantable Condos: These do not meet standard agency guidelines. This might be due to a single entity owning too many units, pending litigation against the HOA, or a high concentration of commercial space. Financing these requires specialized portfolio loans.

If you have been turned down elsewhere because a building is deemed non-warrantable, do not lose hope. We are experts at providing second opinions on condo financing and can often find creative solutions that other lenders miss.

Key Requirements for Condo Mortgage Financing

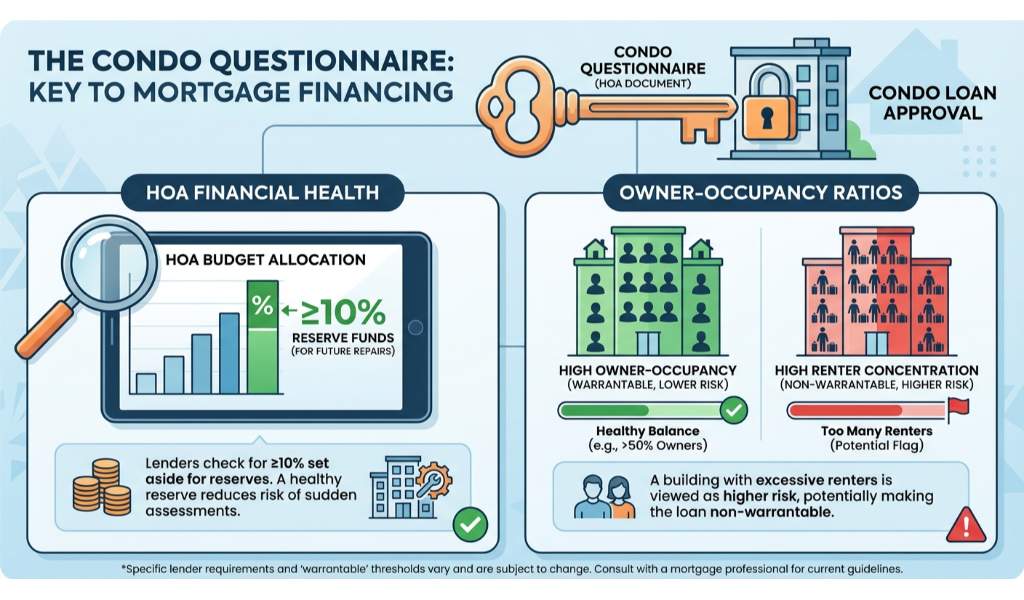

When you apply for condo mortgage financing, lenders look closely at the condominium questionnaire provided by the HOA. This document is the key to unlocking your condo loan. Here is what lenders typically evaluate:

- HOA Financial Health: Lenders want to see that the HOA sets aside at least 10 percent of its budget for reserve funds to cover future repairs.

- Owner-Occupancy Ratios: A building with too many renters can be flagged as a higher risk, potentially making it non-warrantable.

- Insurance Coverage: The master policy must adequately cover the building structure and common areas.

Because these guidelines are complex, getting a second opinion on condo financing is highly recommended. Joe Sauk has been originating mortgage loans since 1993, giving him the deep industry knowledge needed to overcome roadblocks. Whether you are seeking a primary residence in downtown Columbus or a vacation property in Florida, knowing these requirements ensures a smoother closing process.

| Feature | Warrantable Condos | Non-Warrantable Condos |

|---|---|---|

| Loan Types Available | Conventional, FHA, VA | Portfolio Loans, Specialized Non-QM Loans |

| Commercial Space | Typically less than 35% of total square footage | Often exceeds 35% of total space |

| Entity Ownership | No single entity owns more than 20% of units | A single investor or entity owns a large block of units |

| Down Payment | As low as 3% to 5% | Typically requires 10% to 20% or more |

Why Choose Sauk Mortgage Group for Your Columbus Condo Loan?

Choosing the right mortgage broker in Columbus, OH, can make all the difference when securing condo mortgage financing. At Sauk Mortgage Group, our mission is to serve our customers with honesty, integrity, and competence. We shop multiple lenders to find you the lowest interest rates and closing costs available.

We understand that every borrower is unique. Whether you are a first-time homebuyer exploring an FHA purchase loan or a seasoned investor looking to expand your portfolio with an investment property mortgage, we tailor our approach to fit your goals. Do not let a confusing HOA questionnaire stand between you and your dream home. Let us provide the expert guidance you need to navigate the condo market confidently.

Q1: What is condo mortgage financing?

Condo mortgage financing is a specific type of home loan used to purchase a condominium. It requires lenders to evaluate both the borrower’s financial health and the financial stability of the condominium association.

Q2: What does it mean if a condo is non-warrantable?

A non-warrantable condo does not meet the standard lending guidelines set by Fannie Mae or Freddie Mac. This usually happens due to high commercial space, pending HOA litigation, or low owner-occupancy rates, requiring specialized portfolio loans.

Q3: Can I get an FHA loan for a condo in Columbus, OH?

Yes, you can use an FHA purchase loan for a condo, provided the condominium complex is on the FHA approved list or meets the requirements for a single-unit approval (SUA).

Q4: Why should I get a second opinion on condo financing?

Condo loan guidelines are strict and vary by lender. If one lender denies your application because of HOA issues, an experienced broker like Sauk Mortgage Group can often find alternative lenders with more flexible guidelines.

Q5: Do condo loans require a higher down payment?

Not necessarily. If the condo is warrantable, you can secure conventional fixed-rate mortgages with down payments as low as 3 percent. However, non-warrantable condos typically require larger down payments.

Related Posts