Why Choose a 30-Year Fixed-Rate Mortgage? When it comes to buying a home or refinancing…

How to Prepare for Aging Roof Issues and Your Insurance Needs When House Shopping

Finding the perfect home in Columbus, OH is an exhilarating experience. You fall in love with the layout, the neighborhood, and the backyard potential. But there is one feature that often flies under the radar until the home inspection or the insurance quote comes back: the roof.

In the current real estate market, an aging roof is more than just a future repair bill; it is a critical factor that can derail your mortgage approval and make securing homeowners insurance significantly more difficult. Whether you are a first-time homebuyer looking in Grandview Heights or upgrading to a larger family home in Dublin, understanding the intersection of roof condition, mortgage requirements, and insurance insurability is vital.

At Sauk Mortgage Group, we believe in guiding our clients through every hurdle of the home buying process. This guide will help you navigate the complexities of buying a home with an older roof and ensure your investment is protected.

The Hidden Risks of an Aging Roof in Ohio

In Ohio, our weather is notoriously unpredictable. From the heavy snow loads of winter to the severe wind and hail storms of spring, a roof in Columbus takes a beating. When you are house shopping, a roof that is “15 to 20 years old” might sound like it has life left, but insurance carriers and mortgage underwriters may see it differently.

An aging roof poses three primary risks to a transaction:

- Insurability: Many insurance companies are tightening their guidelines, refusing to write new policies on roofs older than 15–20 years without a thorough inspection or a policy exclusion.

- Mortgage Approval: Certain loan programs, specifically government-backed loans, have strict safety and soundness requirements regarding the roof’s condition.

- Financial Burden: If coverage is limited to “Actual Cash Value” (ACV), you could be on the hook for thousands of dollars if a storm hits shortly after closing.

How Roof Condition Affects Your Mortgage Approval

Before you can get the keys, you need to clear the mortgage underwriting process. As an experienced mortgage broker in Columbus, OH, Joe Sauk has seen how roof issues can pause a closing. The impact depends largely on the type of loan you are applying for.

FHA and VA Loan Requirements

Government-backed loans, such as FHA (Federal Housing Administration) and VA (Veterans Affairs) loans, have stricter appraisal standards regarding the property’s condition. The appraiser is required to look for:

- Missing or curled shingles.

- Signs of leakage or moisture damage in the attic.

- Evidence that the roof has less than two to three years of remaining physical life.

If the appraiser flags the roof, the underwriter will likely require the roof to be repaired or replaced before the loan can close. This can create a negotiation standoff between buyer and seller.

Conventional Loan Requirements

Conventional loans are generally more lenient regarding condition than FHA or VA loans. However, the appraiser will still note if the roof is in “poor” condition. More importantly, conventional lenders require proof of homeowners insurance to close. If you cannot find an insurance carrier willing to cover the home because of the roof’s age, the lender cannot fund the loan.

The Insurance Dilemma: Replacement Cost vs. Actual Cash Value

One of the biggest shocks for homebuyers in Columbus today is the shift in how insurance companies cover older roofs. When shopping for insurance, you will encounter two main types of coverage. Understanding the difference is crucial for your financial safety.

Table: Comparing Roof Insurance Coverage Types

| Feature | Replacement Cost Value (RCV) | Actual Cash Value (ACV) |

|---|---|---|

| Definition | Pays to replace the roof with new materials at today’s prices, without deduction for depreciation. | Pays the replacement cost minus depreciation based on the roof’s age. |

| Best For | Homeowners who want full financial protection. | Homeowners with older roofs who cannot qualify for RCV or want lower premiums. |

| Out-of-Pocket Cost | Typically limited to your deductible. | Deductible + the depreciated value (can be thousands of dollars). |

| Availability | Usually available for roofs under 10-15 years old. | Common default for roofs over 15-20 years old. |

The Trap: If you buy a home with a 20-year-old roof and accept an ACV policy, and a hail storm destroys the roof two months later, the insurance check might only cover 20% of the cost to replace it. You would be responsible for the rest.

Steps to Protect Yourself When House Shopping

Don’t let a roof issue kill your dream of homeownership. Here is a strategic roadmap to handling aging roofs when looking at homes in Franklin County and surrounding areas.

1. Look Up, Then Look Closer

When touring a home, do a visual check from the ground. Look for granular loss (bald spots on shingles), curling edges, or moss growth. Inside, check the ceilings and the attic for water stains. However, a visual check isn’t enough.

2. Get a Specialized Roof Inspection

General home inspectors are fantastic, but they are generalists. If the roof is flagged as “aging” or “near end of life,” hire a licensed roofing contractor to provide a specific inspection and a certification of remaining life (often required by lenders). This costs a little extra but provides the leverage you need for negotiations.

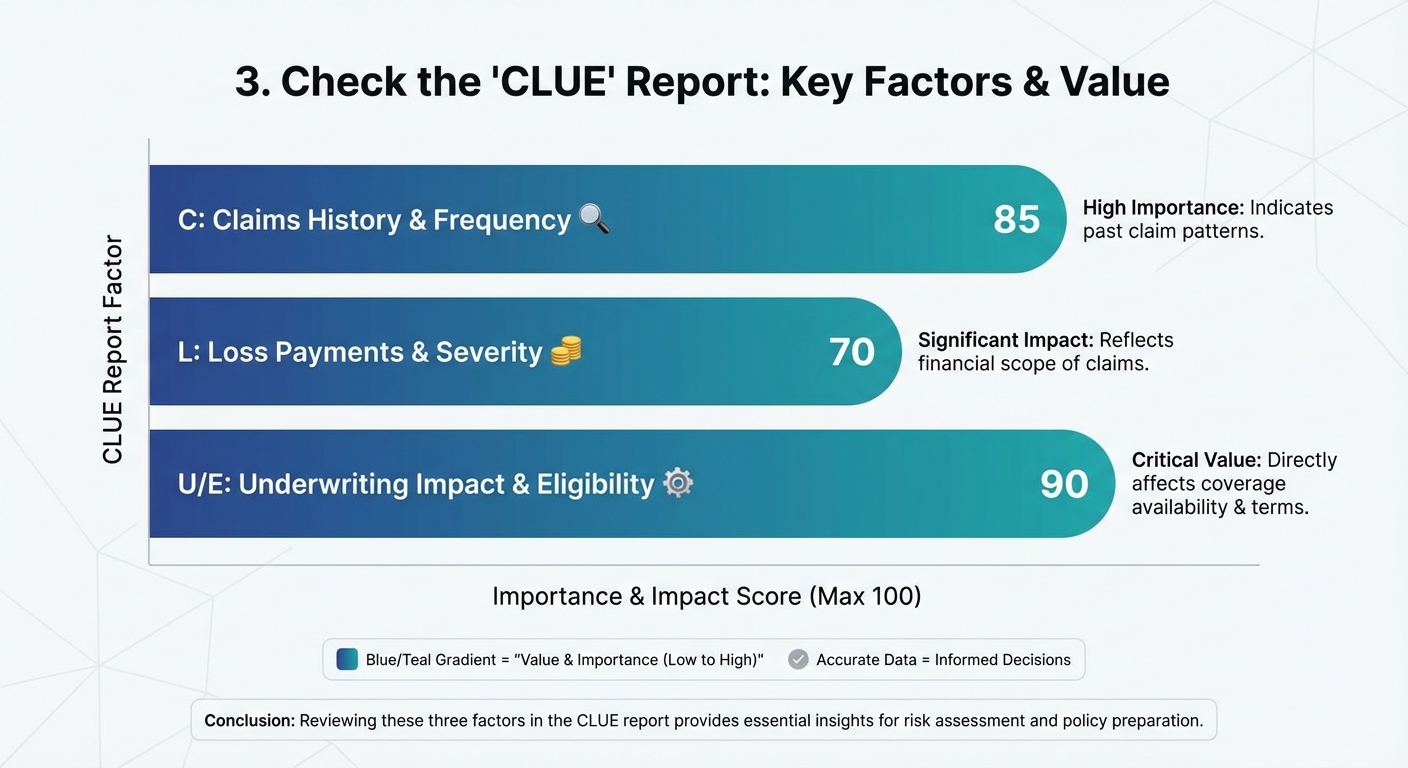

3. Check the “CLUE” Report

4. Secure Insurance Quotes Early

Do not wait until the week before closing to shop for insurance. As soon as you go into contract, call insurance agents. Give them the specific age of the roof. If three carriers decline coverage or only offer ACV, you have a major bargaining chip to take back to the seller.

Strategies for Financing a Home with a Bad Roof

If you find the perfect house in the perfect Columbus neighborhood, but the roof is shot, you still have options. At Sauk Mortgage Group, we help clients overcome these roadblocks with creative financing solutions.

Negotiate a Seller Concession

You can ask the seller to replace the roof prior to closing. If they don’t have the cash, it can sometimes be paid out of the proceeds of the sale at the closing table (contractor gets paid directly by the title company). Alternatively, the seller can offer a credit towards your closing costs, freeing up your cash to pay for the roof post-closing (though the lender must approve this, and the roof usually must be watertight to close).

Renovation Loans

If the seller refuses to fix it and the roof is too far gone for a standard loan, consider a renovation loan. Programs like the FHA 203(k) or Fannie Mae HomeStyle allow you to wrap the cost of the roof replacement (and other upgrades) into your mortgage. You buy the house “as-is,” and the repairs are completed after closing using the loan funds.

Thinking about a fixer-upper? Contact Joe Sauk to discuss renovation loan options tailored to your budget.

Local Factors: Why Columbus Roofs Age Faster

When buying in Central Ohio, it is important to understand our specific micro-climate. We experience:

- Freeze-Thaw Cycles: Water gets into small cracks in shingles, freezes, expands, and widens the cracks.

- Wind Damage: Ohio allows for “matching” in insurance claims (if they can’t match the shingle, they may have to replace the whole slope or roof), but older discontinued shingles make this tricky.

- Algae Growth: Humid Columbus summers can lead to algae streaks, which are mostly cosmetic but can signal moisture retention.

Frequently Asked Questions (FAQs)

1. Can I buy a house with a roof that needs to be replaced immediately?

It depends on the loan type. For FHA and VA loans, the roof generally must be replaced before closing if it leaks or has less than two years of life. For conventional loans, you might be able to close if the roof is not leaking, but you may face insurance difficulties. A renovation loan is often the best solution in this scenario.

2. Will my mortgage lender require a roof inspection?

Not always. The appraiser will do a visual observation. If the appraiser notes significant damage, deterioration, or signs of leakage, the underwriter will then require a professional roof inspection to determine if the roof is serviceable.

3. What if the seller refuses to fix the roof?

If the roof condition prevents financing (e.g., an FHA appraisal requirement) and the seller refuses to fix it, the deal may fall through. However, you can switch to a renovation loan (FHA 203k) to buy the home as-is and finance the repairs, provided the seller agrees to the price and timeline.

4. How do I know the age of the roof?

Ask the seller for the receipt or warranty from the last replacement. If they don’t know, look at the building permit history for the property, which is often available online through the local county or city building department in Columbus and surrounding suburbs.

5. Is a roof certification worth the cost?

Yes. A roof certification is a professional opinion from a roofer stating the roof has a specific remaining life expectancy (e.g., 3-5 years). This document can sometimes satisfy an underwriter’s concerns or help you secure better insurance coverage.

Secure Your Investment with Sauk Mortgage Group

Buying a home is one of the largest financial decisions you will make. Don’t let an aging roof surprise you at the closing table or result in a denied insurance claim down the road. By understanding the condition of the property and aligning it with the right financing strategy, you can buy with confidence.

Whether you are looking for a standard Conventional loan, an FHA loan for a first-time purchase, or a specialized solution for a property that needs a little love, Sauk Mortgage Group is here to help. Joe Sauk has been serving Columbus, OH homeowners since 1993 with honesty, integrity, and competence.

Ready to explore your mortgage options?

Get Your Personalized Quote Today

Call Joe directly at (614) 353-5088 or email joe@saukmortgagegroup.com to start your journey.

Related Posts