Navigating First-Time Buyer Loans with Confidence Buying your first property is an exciting milestone, but…

Your Complete Guide to a HELOC Home Equity Line of Credit in Columbus, OH

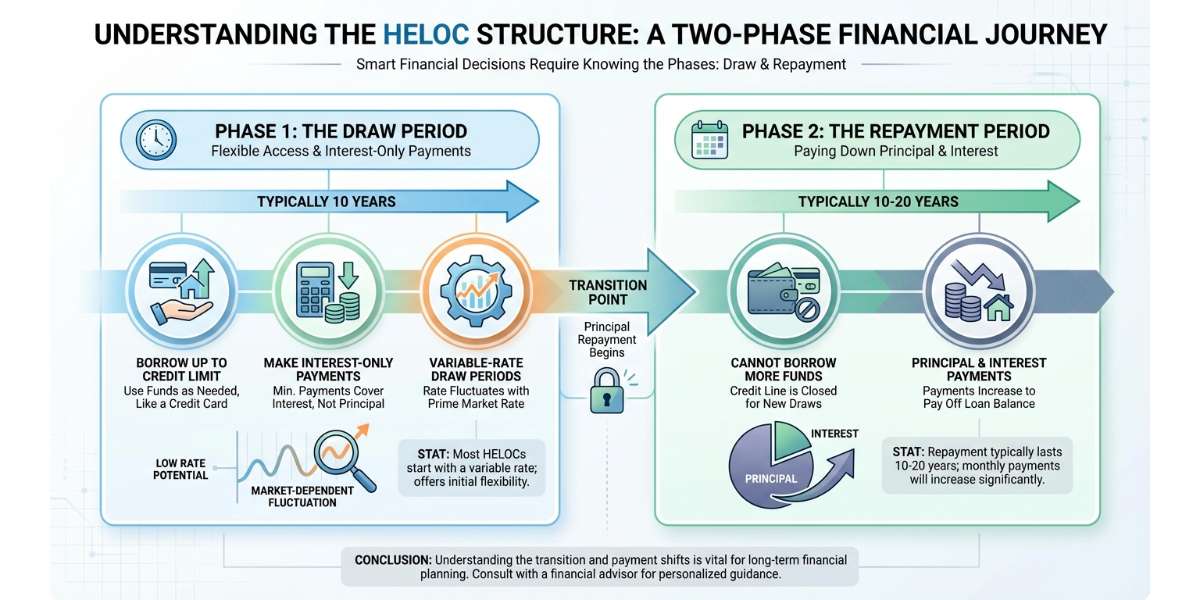

What is a HELOC and How Does It Work?

If you are a homeowner in Columbus, Ohio, you might be sitting on a significant amount of untapped wealth. A HELOC home equity line of credit is a powerful financial tool that allows you to borrow against the equity you have built in your property. Unlike a traditional lump-sum loan, a HELOC operates much like a credit card. You are given a maximum credit limit, and you can draw from it as needed, paying interest only on the amount you actually use.

Many homeowners use a HELOC for major expenses such as home renovations, debt consolidation, or funding higher education. When exploring your borrowing options, it is important to understand how a HELOC compares to a home equity loan or second mortgage. While a traditional home equity loan provides a single lump sum with a fixed rate, a HELOC offers ongoing flexibility.

At Sauk Mortgage Group, led by broker-owner Joe Sauk, we specialize in helping local homeowners navigate these choices. We are experts at providing second opinions on HELOCs to ensure you are getting the most favorable terms available in the market.

Variable-Rate vs. Fixed-Rate Draw Periods Explained

Understanding the structure of a HELOC home equity line of credit is crucial for making smart financial decisions. A standard HELOC is divided into two phases: the draw period and the repayment period. During the draw period, which typically lasts 10 years, you can borrow funds up to your credit limit and make interest-only payments.

- Variable-Rate Draw Periods: Most HELOCs start with a variable interest rate. This means your rate will fluctuate based on the prime market rate. While this offers immense flexibility and often lower initial rates, your monthly payments can change over time.

- Fixed-Rate Draw Periods: Some lenders offer the option to convert a portion or all of your outstanding HELOC balance into a fixed-rate loan. A fixed-rate draw period provides predictable, stable monthly payments, protecting you from future interest rate hikes.

Depending on your financial goals, you might also want to compare these options against a cash-out refinance. A cash-out refinance replaces your primary mortgage entirely, which can be beneficial if current market rates are lower than your existing mortgage rate. If you are unsure which path is right for you, bringing your current offers to Joe Sauk for a professional second opinion can save you thousands of dollars over the life of your loan.

| Feature | Variable-Rate HELOC | Fixed-Rate Option HELOC | Cash-Out Refinance |

|---|---|---|---|

| Interest Rate | Fluctuates with the market | Locked in for a set balance | Fixed for the entire new mortgage |

| Funds Access | Revolving line of credit | Revolving, but locked portions are fixed | Lump sum at closing |

| Payment Style | Interest-only during draw period | Predictable principal and interest | Standard monthly mortgage payment |

| Best For | Ongoing projects and flexible spending | Stability while retaining credit access | Large, single expenses and lower overall rates |

Why Get a Second Opinion on Your HELOC in Ohio?

Securing a mortgage product is a major financial commitment. Even if you have already received an offer from your primary bank, getting a second opinion on your HELOC is a smart move. Different lenders have different risk appetites, margin requirements, and promotional rates.

Joe Sauk has been originating mortgage loans in Columbus, OH since 1993. As an independent mortgage broker, Sauk Mortgage Group shops multiple lenders to find the exact right fit for your unique situation. Our mission is to serve our customers with honesty, integrity, and competence. Whether you are leaning toward a variable-rate HELOC, a fixed-rate option, or another equity-tapping strategy, we will review your current quotes, explain the fine print, and help you overcome any roadblocks. We pride ourselves on securing the lowest interest rates and closing costs available for our clients.

Q1: What exactly is a HELOC home equity line of credit?

A HELOC is a revolving line of credit secured by the equity in your home. It functions similarly to a credit card, allowing you to borrow money as needed up to a certain limit, pay it back, and borrow again during the draw period.

Q2: How long does the draw period last on a typical HELOC?

The draw period for a standard HELOC usually lasts for 10 years. During this time, you can access your funds and typically only need to make minimum interest payments.

Q3: Can I get a fixed interest rate on my HELOC?

Yes. While HELOCs generally feature variable interest rates, many lenders offer a fixed-rate option that allows you to lock in the interest rate on a specific portion of your outstanding balance for predictable monthly payments.

Q4: How does a HELOC differ from a cash-out refinance?

A HELOC is a second mortgage that acts as a line of credit, leaving your primary mortgage untouched. A cash-out refinance replaces your existing first mortgage with a brand new, larger loan, giving you the difference in a lump sum of cash.

Q5: Why should I get a second opinion on my HELOC offer?

Rates, fees, and terms can vary wildly between lenders. Getting a second opinion from an experienced mortgage broker like Joe Sauk ensures you are not overpaying on hidden fees or accepting a higher interest rate than you qualify for.

Related Posts