Unlocking Homeownership with Good-Neighbor Community-Service Homebuying Programs Teachers, firefighters, police officers, and other public servants…

Your Complete Guide to a First-Time Homebuyer Mortgage in Columbus, OH

Navigating First-Time Buyer Loans with Confidence

Buying your first property is an exciting milestone, but securing the right financing is the true foundation of a successful real estate journey. Whether you are actively searching for a first time homebuyer mortgage or simply exploring your options for First-Time Buyer Loans, knowing what is available to you makes all the difference. At Sauk Mortgage Group in Columbus, OH, we specialize in helping new buyers navigate the complex world of home financing.

A First-Time Home Buyer Mortgage is specifically designed to remove the common barriers to homeownership. These programs typically feature lower down payment requirements, reduced mortgage insurance costs, and flexible credit guidelines. Working directly with local mortgage broker Joe Sauk ensures you have an expert in your corner to shop multiple lenders and find the exact loan structure that fits your financial goals. Furthermore, if you already have a quote from another lender, do not hesitate to reach out. We are experts at providing second opinions on first-time homebuyer mortgages to make sure you are getting the best possible terms.

Comprehensive Coverage: HomeReady and Home Possible

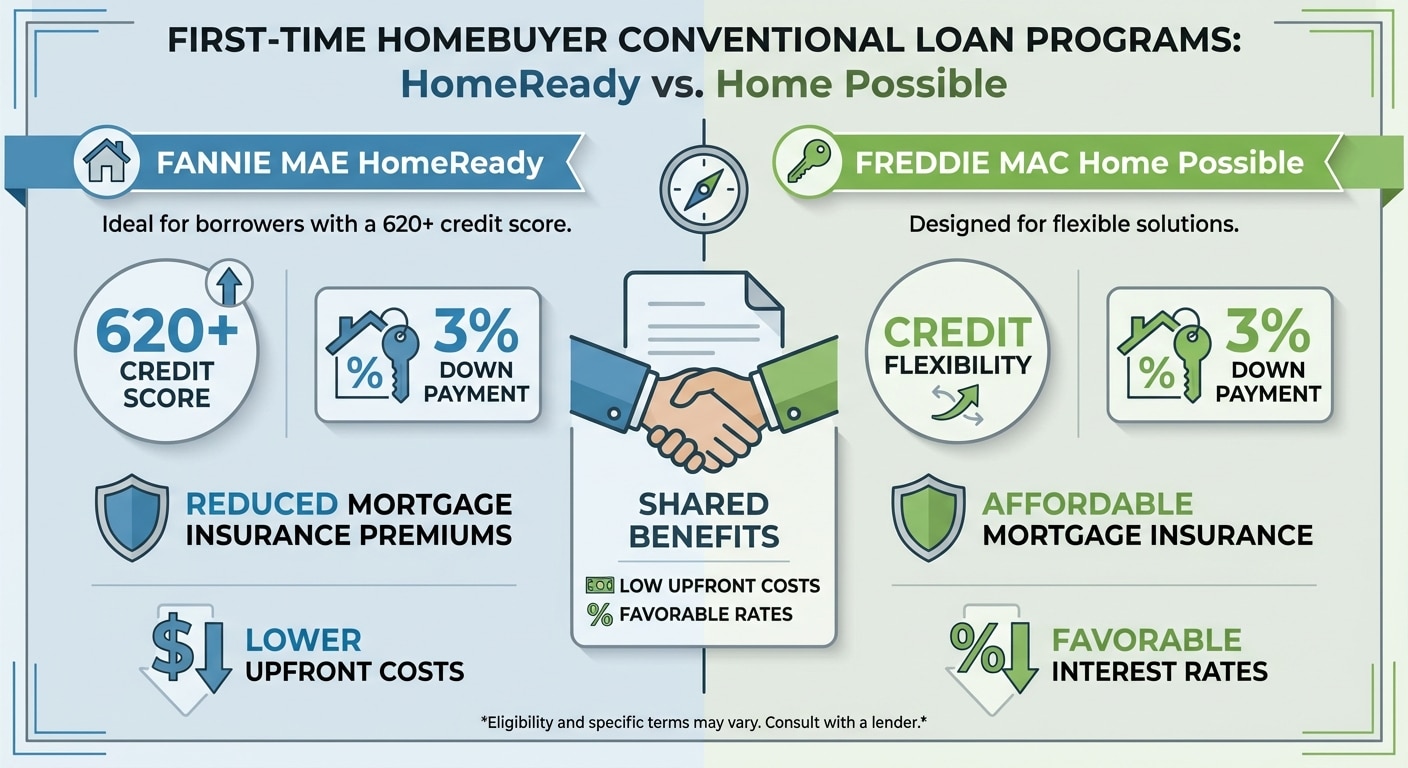

When exploring a first time homebuyer mortgage, two of the most popular conventional loan programs are Fannie Mae’s HomeReady and Freddie Mac’s Home Possible. Both programs are tailored for buyers who want to keep their upfront costs as low as possible without sacrificing favorable interest rates.

- HomeReady: Ideal for borrowers with a credit score of 620 or higher. This program allows for a down payment as low as 3 percent and offers reduced mortgage insurance premiums.

- Home Possible: Designed to offer maximum flexibility, this program also requires just 3 percent down and is highly accommodating for multi-generational households pooling their resources.

One of the greatest advantages of both HomeReady and Home Possible is their compatibility with other financial aids. Buyers can easily pair these loans with down payment assistance programs to cover upfront costs. Depending on your credit profile, it is also wise to compare these conventional options against an FHA purchase loan to determine which route offers the most affordable monthly payment for your Columbus home.

| Loan Program | Minimum Down Payment | Minimum Credit Score | Best For |

|---|---|---|---|

| HomeReady | 3% | 620 | Buyers with low to moderate income and good credit |

| Home Possible | 3% | 660 | Buyers needing flexible sources of funds for a down payment |

| FHA Loan | 3.5% | 580 | Buyers with lower credit scores needing relaxed underwriting guidelines |

The Value of a Second Opinion on Your Mortgage

Getting a second opinion on your mortgage is one of the smartest financial moves you can make as a new buyer. A minor difference in interest rates or closing costs can save you thousands of dollars over the life of your loan. Unfortunately, many buyers accept the very first offer they receive without realizing they might qualify for better First-Time Buyer Loans elsewhere.

At Sauk Mortgage Group, we pride ourselves on transparency and borrower education. We will review your current pre-approval, break down the hidden fees, and leverage our network of lenders to see if we can secure a better rate or structure for your First-Time Home Buyer Mortgage. Let our decades of experience in the Columbus, OH market work to your advantage so you can purchase your dream home with absolute confidence.

Q1: What qualifies as a first time homebuyer mortgage?

A first time homebuyer mortgage is typically designed for individuals who have not owned a principal residence in the past three years. These programs feature lower down payment requirements and flexible credit guidelines tailored to new buyers.

Q2: How much down payment do I need for First-Time Buyer Loans in Columbus, OH?

Many first-time buyer programs, such as HomeReady and Home Possible, require as little as 3 percent down. Other options like FHA loans require a minimum of 3.5 percent.

Q3: What is the main difference between HomeReady and Home Possible?

Both are excellent conventional loan options requiring minimal down payments. HomeReady is backed by Fannie Mae and favors borrowers with credit scores of 620 or higher. Home Possible is backed by Freddie Mac and offers unique flexibility for multi-generational households.

Q4: Can I use outside funds to help cover my down payment?

Yes! Both HomeReady and Home Possible allow you to use gifted funds from family members. You can also combine these loans with local down payment assistance programs to significantly reduce your out of pocket expenses.

Q5: Why should I get a second opinion on my mortgage offer?

Different lenders offer different rates, fees, and loan structures. We are experts at providing second opinions on first-time homebuyer mortgages to ensure you are not overpaying on closing costs or interest rates.

Related Posts