Finding the perfect home in Columbus, OH is an exhilarating experience. You fall in love with the…

AI Predictions for the 2026 Mortgage Market in Columbus, OH

Columbus, OH

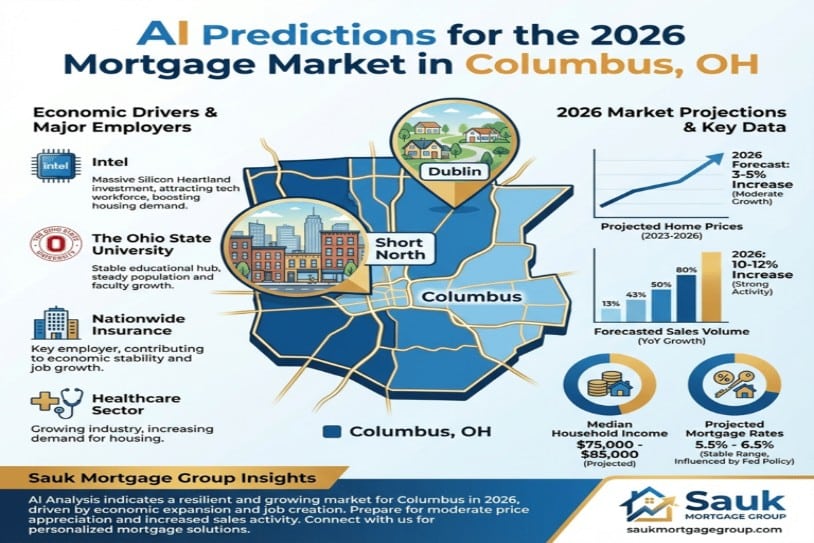

Columbus, the heart of Ohio’s innovation corridor, closed out 2025 on a high note with fall sales showing renewed vigor – up 5% from summer lows – as Federal Reserve rate cuts began to permeate the local lending scene. Fueled by Intel’s massive semiconductor plant in New Albany, a booming logistics sector, and the enduring draw of Ohio State University’s ecosystem, this Central Ohio powerhouse blends affordability with urban energy, from the eclectic Short North to family havens in Dublin. As we turn to 2026, a synthesis of forecasts from the National Association of Realtors (NAR), Mortgage Bankers Association (MBA), Fannie Mae, and regional data from Columbus Realtors, the Ohio Housing Needs Assessment (HNA), and Zillow reveals a market poised for balanced expansion. This detailed forecast breaks down rate movements, price appreciations, sales and origination surges, and Columbus-specific levers – like workforce influxes and neighborhood revitalizations – to equip Buckeye buyers, refinancers, and investors with the insights needed to thrive in this resilient Midwest gem.

National Mortgage Rate Trends Shaping 2026

The U.S. mortgage landscape enters 2026 with rates easing incrementally, providing a welcome tailwind for affordability without overpromising a return to rock-bottom figures. Fannie Mae’s Economic and Housing Outlook projects the 30-year fixed-rate mortgage averaging 6.3% throughout the year, gradually declining to 5.9% by December as the Federal Reserve’s funds rate stabilizes near 3% and core inflation moderates to around 2%. NAR Chief Economist Lawrence Yun concurs, forecasting an overall average of 6%, down from 6.7% in 2025, though he cautions of potential upside to 6.5% if supply chain tariffs or energy volatility reignite inflationary pressures. The MBA’s latest survey aligns, anticipating rates in the 6-6.5% corridor, with adjustable-rate mortgages (ARMs) poised for a breakout: Resets from 2025 originations could push effective rates below 6%, catalyzing a 20-25% refinance uptick as 10-year Treasury yields hold steady near 4%.

For Columbus borrowers, this national softening amplifies local advantages. Ohio’s conforming loan limit of $832,750 covers most transactions, but the city’s growing jumbo segment – driven by $400,000+ homes in upscale areas like Worthington – may favor 5/6 ARMs for tech transplants from California. Brokers should highlight temporary buydowns, especially as Columbus’s median household income ($86,880+) supports payments but leaves little room for surprises amid 2-3% annual property tax escalations.

Home Prices and Sales Volume: Sustainable Gains in the Midwest Heartland

Nationally, the stage is set for a rebound without exuberance. NAR projects median existing-home prices to climb 4% in 2026, following a 3% rise in 2025, while sales volumes surge 14% to approximately 5.3 million units – the end of three consecutive years of decline – as pent-up demand from millennials and Gen Z finally unleashes. Fannie Mae’s revised outlook tempers this to 7.3% sales growth and a modest 0.4% price increase in their Home Value Index, reflecting regional variations but underscoring Midwest resilience. Zillow’s forecast flips positive, anticipating 0.4% national appreciation over the next 12 months, with Ohio markets like Columbus leading due to job-driven migration. HomeLight ranks Ohio among the hottest 2026 housing markets, citing low inventory and strong wage growth as catalysts.

Columbus exemplifies this optimism: The Columbus Realtors’ 2025 year-end report shows medians at $320,000, up 4.2% year-over-year, with 2026 projections from local experts like Thomas Riddle calling for 3-5% appreciation to $329,000-$336,000, supported by 10,000+ new jobs from Intel and Amazon expansions. Sales could rise 10-12%, with days on market shortening to 25-35 from 45, as inventory builds to 3-4 months’ supply – easing the seller’s edge in hot spots like German Village or the Arena District. Starter homes under $250,000 may see 2-3% gains, while luxury segments in New Albany push 5%, though overbuilding in multifamily could soften condo prices by 1%. The Ohio HNA highlights persistent affordability for first-timers, with 30% of sales from this group leveraging state down payment assistance.

Mortgage Originations: A Purchase-Dominated Revival

Origination activity emerges as 2026’s standout story, with the MBA forecasting an 8% increase in single-family volumes to $2.2 trillion, alongside a 7.6% rise in loan counts to 5.8 million – 80% driven by purchases as buyers acclimate to 6% rates. Fannie Mae ups the ante to $2.32 trillion total, with refinances expanding to 20% of the mix thanks to ARM adjustments and equity harvesting. iEmergent’s analysis projects even stronger 13% growth to $2.27 trillion, emphasizing non-bank lenders’ role in digital efficiencies.

In Columbus, this national momentum translates to 10-12% local origination growth, bolstered by Franklin County’s economic engine – adding 15,000 jobs in IT and manufacturing. Conforming loans will dominate 85% of the pipeline for $300,000 medians, but jumbos could surge 8-10% for $500,000+ properties in upscale suburbs like Upper Arlington. FHA and VA products, popular among military families near Rickenbacker Air Base, may see 25% uptake, while first-time buyers tap Ohio Housing Finance Agency programs for 3-5% down payments.

Affordability and Buyer Sentiment in Focus

Affordability metrics improve nationally, with home-price-to-income ratios dipping to 5.5x, but Columbus shines brighter at around 4.8x – making a $320,000 home’s $1,900 monthly payment at 6% accessible for $80,000 median earners, though rising utilities and 2% property taxes nibble at edges. The Ohio HNA warns of increasing mortgage burdens for lower-income households, yet buyer sentiment remains robust: 60% of Midwest respondents in NAR surveys plan purchases within two years, with Columbus drawing 20% of its demand from out-of-state relocators seeking value versus coastal costs. Millennials and Gen Z, comprising 35% of activity, target vibrant areas like Italian Village, while empty-nesters (15%) downsize amid equity booms – though 22% of renewals face payment shocks, urging proactive switches to fixed terms.

Emerging Trends: Technology and Sustainability

Digital transformation takes center stage: AI-driven underwriting could slash approval times to 7-10 days, with 40% of closings fully virtual, per MBA trends. In Columbus, blockchain for title transfers will streamline deals near the Scioto River. Sustainability gains ground: Green mortgages offering 0.125-0.25% rate discounts for energy-efficient upgrades may capture 15% of originations, aligning with Ohio’s incentives for solar and EV infrastructure – particularly relevant for flood-prone zones in Franklinton.

Key Challenges on the Horizon

Supply constraints persist, with new construction lagging 10-12% behind demand due to labor shortages and zoning debates. Regulatory shifts, like potential FHA credit score overlays, could sideline 5% of applicants. Locally, Columbus contends with 8-10% insurance premium hikes from severe weather risks, as seen in recent tornadoes, and infrastructure strains from population growth – potentially delaying 7% of listings. Geopolitical factors, including trade tariffs, loom as a 0.25% rate adder.

Looking Ahead: Columbus’s Dynamic Ascent

2026 solidifies Columbus as a Midwest mortgage success story, with easing rates, surging volumes, and controlled prices creating fertile ground for opportunity. For brokers and borrowers alike, the year underscores the power of preparation – leveraging digital tools, green incentives, and local job waves to navigate hurdles. As the Buckeye State’s capital evolves, staying ahead of these trends will turn predictions into personalized paths to homeownership.

Related Posts