Why 2026 is the Prime Time for Columbus Homeowners to Tap Into Equity As we…

Refinancing Your Mortgage: The Cost of Waiting in Today’s Market

As we wrap up 2025, many homeowners in Columbus, OH, and across Ohio and Florida are asking the same question: Should I refinance my mortgage now, or wait for rates to drop further?

It’s a smart question. Mortgage rates have stabilized after years of volatility, hovering around the mid-6% range for 30-year fixed loans. But waiting for that “perfect” lower rate comes with a real cost – one that adds up quickly in extra interest payments.

At Sauk Mortgage Group, we’ve helped hundreds of clients navigate refinancing decisions with honesty and clarity. Led by Joe Sauk, with over 30 years of experience originating loans, our team focuses on finding ideal financing solutions tailored to your unique situation. Whether you’re looking to lower your monthly payment, shorten your loan term, or tap into your home equity, we’re here to guide you through a stress-free process.

In this guide, we’ll break down the true cost of waiting, share real-world examples, and explain why acting now could save you thousands – while rates remain steady and competitive.

Current Mortgage Rates and the 2025-2026 Outlook

As of mid-December 2025, average 30-year fixed mortgage rates sit around 6.2% to 6.3%, according to sources like Freddie Mac and Mortgage News Daily. Refinance rates are similar, often slightly higher depending on your credit profile and loan type.

This is a significant improvement from the 7%+ rates many homeowners locked in during 2022-2024. Yet, some are holding out, hoping for rates to dip into the 5% range or lower in 2026.

Expert forecasts suggest rates will remain relatively steady or decline only modestly. Many analysts predict averages between 5.9% and 6.2% through 2026, with gradual easing tied to inflation and economic growth. Dramatic drops aren’t widely expected soon.

The reality? No one can predict rates with certainty. If you’re waiting for a big decline that may not arrive – or arrives later than expected – you’re paying higher interest every month in the meantime.

The Real Cost of Waiting: A Closer Look with Examples

Let’s make this concrete with some numbers. (These are illustrations – your exact savings depend on your loan balance, credit, and other factors. Use our free mortgage calculator for personalized estimates.)

Example 1: Rate-and-Term Refinance to Lower Your Payment

Assume you have a $400,000 remaining balance on a 30-year fixed loan at 7.0% (common for loans originated in recent years).

- Current monthly payment (principal & interest): Approximately $2,661

- Refinance to 6.25% today: New payment ≈ $2,462

- Monthly savings: About $199

If you wait just one year hoping for lower rates:

- Extra interest paid: Roughly $2,400 (not counting principal reduction)

- Total cost of waiting one year: $2,400+ in lost savings

Now, if rates drop to 5.75% in a year (an optimistic scenario), your payment could drop to ≈ $2,334 – additional savings of $128/month. But you’d have already “spent” $2,400 waiting. It could take years to recoup that through slightly lower future payments.

Example 2: Higher Original Rate Scenario

If your current rate is 7.5% on a $300,000 balance:

- Current payment: ≈ $2,098

- Refi to 6.25%: ≈ $1,847

- Monthly savings: $251

Waiting six months costs about $1,500 in extra interest. Closing costs for a refinance typically range from $5,000–$10,000 (depending on loan size and options like appraisal waivers). With $251/month savings, you’d break even in 20–40 months – well worth it if you plan to stay in the home.

The bottom line: Every month you delay locks in higher payments longer, eroding your potential savings.

Beyond the Numbers: Other Costs of Waiting

Financial costs aren’t the only factor. Waiting can mean:

- Missed opportunities to build equity faster – Lower payments let you pay down principal sooner or switch to a 15- or 20-year term.

- Risk of rates rising – Economic shifts could push rates up, making today’s levels look attractive in hindsight.

- Life changes – Job relocation, family growth, or rising expenses might make refinancing harder later.

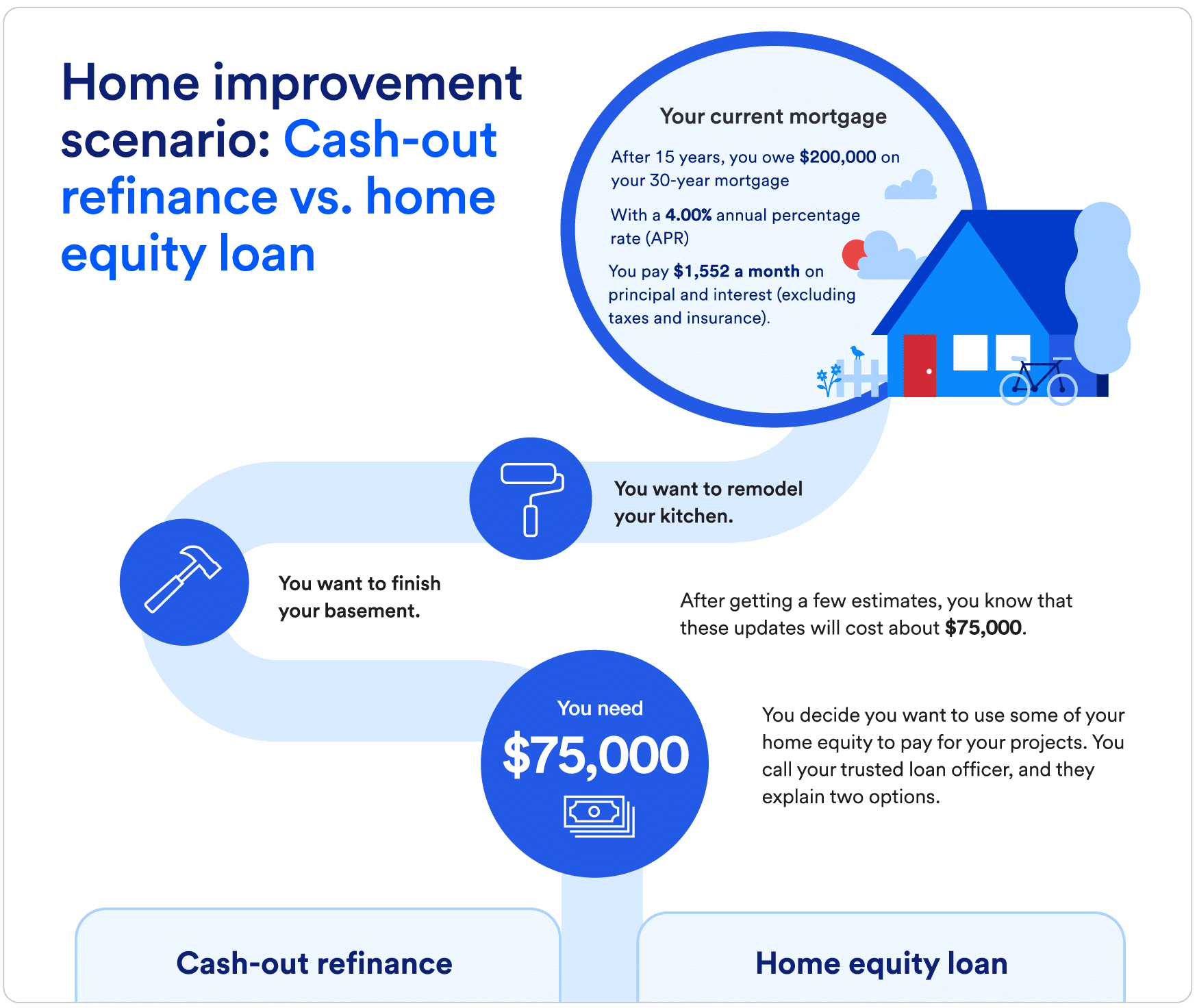

- Home equity goals – Delaying a cash-out refinance could mean missing chances to consolidate high-interest debt, fund renovations, or #CreateMemories with home improvements.

At Sauk Mortgage Group, we specialize in overcoming roadblocks – like unique income sources, credit challenges, or documentation hurdles – so you can maximize your benefits without unnecessary delays.

Why Sauk Mortgage Group Makes Refinancing Stress-Free

As a local mortgage broker in Columbus, OH (serving all of Ohio and Florida), we shop multiple lenders to secure the lowest possible rates and ideal terms. Unlike big banks, we offer:

- Fast closings

- Personalized guidance from seasoned loan officers

- Options like buydowns, appraisal waivers, and no-escrow accounts

- A full menu of refinance products, including Conventional, FHA, VA, Jumbo, and more

Our team – backed by great people and 100% customer-focused – includes Joe Sauk (NMLS #589820), Amy Sauk, and experts with decades of experience. We’re committed to outstanding customer service from your first conversation to closing.

Check today’s rates or get a no-obligation quote in minutes.

Is Refinancing Right for You? Take the Next Step Today

Refinancing isn’t always the best choice for everyone, but with rates steady and savings potential high for many homeowners, the cost of waiting is worth calculating.

Don’t let hesitation stand between you and lower payments, more equity, or financial flexibility. Contact us today – call or text Joe directly at (614) 353-5088, get a quote, or start your application online.

We’re here to provide clear answers and guide you toward the best decision for your #DreamHome, #BuildEquity, and #ProudToOwn goals.

Sauk Mortgage Group Ltd. | NMLS #1879972 | 1880 Mackenzie Drive, Suite 107, Columbus, OH 43220

Rates and programs subject to change. This is not a commitment to lend. Consult a loan officer for details.

Related Posts