Understanding the FHA Streamline Refi Process If you currently have an FHA loan in Columbus,…

The Complete Guide to Getting an Energy-Efficient Mortgage in Columbus, OH

What is an Energy-Efficient Mortgage (EEM)?

Are you looking to buy a home or refinance in Columbus, OH while lowering your utility bills and reducing your carbon footprint? An Energy-Efficient Mortgage (often referred to as a Green Mortgage) might be the perfect solution. This unique financing option allows homebuyers and homeowners to roll the cost of energy-saving improvements directly into their primary home loan.

At Sauk Mortgage Group, led by broker-owner Joe Sauk who has been originating loans since 1993, we specialize in helping local borrowers navigate these specialized loan products. Whether you are upgrading your HVAC system, installing solar panels, or adding high-efficiency insulation, an energy efficient mortgage gives you the buying power to make your home comfortable and eco-friendly. We are also experts at providing second opinions on energy-efficient mortgages to ensure you are getting the best rates and terms possible.

Depending on your financial situation, you can pair an EEM with various loan types. For example, you might consider an FHA purchase loan for lower down payment requirements or a conventional fixed rate mortgage if you have a stronger credit profile.

Exploring FHA, VA, and Conventional EEM Options

Understanding the different types of Green Mortgages is crucial for Columbus homebuyers. Here is a closer look at the primary programs available:

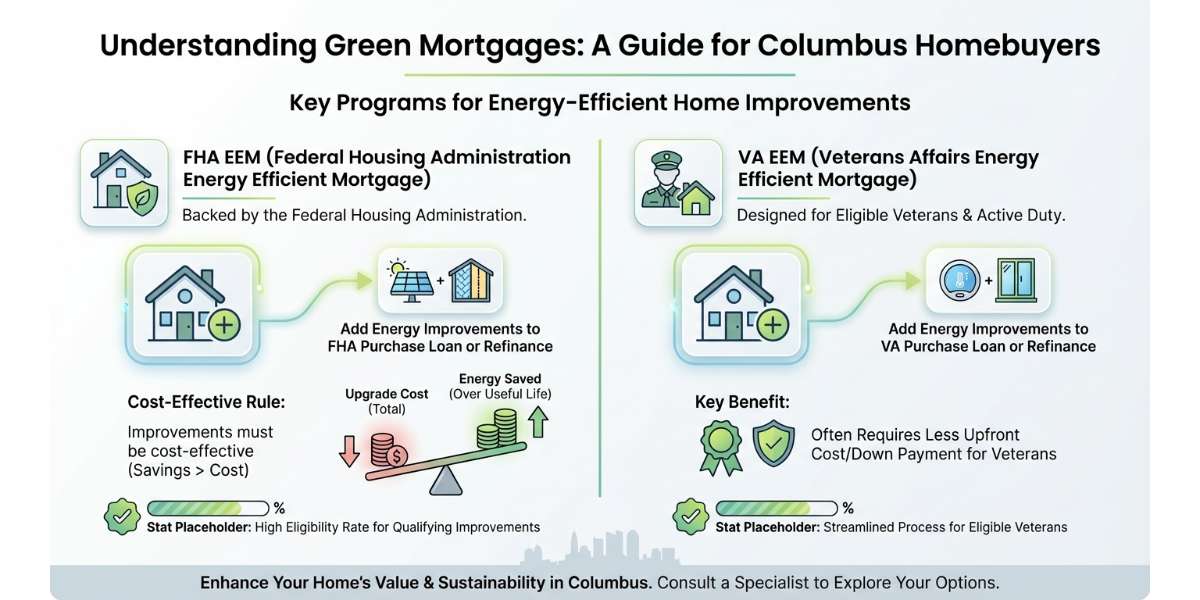

- FHA EEM: Backed by the Federal Housing Administration, this program allows you to add the cost of energy improvements to your FHA purchase loan or refinance. The improvements must be cost-effective, meaning the total cost of the upgrades is less than the total amount of energy saved over their useful life.

- VA EEM: Designed for eligible veterans and active-duty military personnel, the VA Energy-Efficient Mortgage allows borrowers to add up to a specific amount for energy efficiency improvements when purchasing or refinancing a home. It is a fantastic way for military families in Ohio to reduce their long-term living expenses.

- Conventional EEM: Offered through Fannie Mae (HomeStyle Energy) and Freddie Mac (GreenCHOICE), a conventional EEM is ideal for borrowers with strong credit scores. You can bundle your upgrades into a standard conventional fixed rate mortgage, making it a streamlined process for substantial home improvements.

If you have already received a quote from another lender, reach out to us. We are experts at providing second opinions on energy-efficient mortgages and can often find better terms or lower closing costs.

| Loan Type | Best For | Max Upgrade Financing (Approx) | Credit Requirement |

|---|---|---|---|

| FHA EEM | First-time buyers, lower credit scores | Up to 5% of property value | Flexible (Often 580+) |

| VA EEM | Veterans, active military, spouses | $3,000 to $6,000+ (with VA approval) | Flexible (No strict minimum) |

| Conventional EEM | Strong credit, higher down payments | Up to 15% of as-completed value | Good to Excellent (620+) |

Why Choose Sauk Mortgage Group for Your Green Mortgage?

Securing an energy efficient mortgage requires working with a knowledgeable mortgage broker who understands the local Columbus, OH real estate market. Since 1993, Joe Sauk has been dedicated to serving customers with honesty, integrity, and competence. At Sauk Mortgage Group, we shop multiple lenders to find the lowest interest rates and closing costs tailored to your specific goals.

Whether you want to lower your monthly utility bills or increase your property value through sustainable upgrades, we are here to guide you every step of the way. Do not settle for the first offer you receive. Because we are experts at providing second opinions on energy-efficient mortgages, we can review your current pre-approval to ensure you are truly getting the most competitive deal available in Ohio.

Q1: What qualifies as an energy-efficient upgrade for an EEM?

Upgrades typically include new HVAC systems, solar panels, double-pane windows, weatherization, and high-efficiency insulation. A home energy assessment is usually required to verify the cost-effectiveness.

Q2: Can I get an energy-efficient mortgage if I am refinancing my Columbus home?

Absolutely. You can use an EEM for both purchasing a new home and refinancing your current residence to pay for green upgrades.

Q3: Do I need a perfect credit score to qualify for a green mortgage?

Not necessarily. Programs like the FHA EEM have flexible credit requirements, while conventional options may require a higher score. We can help determine which program fits your profile.

Q4: How do I know if the energy savings will cover the upgrade costs?

A certified Home Energy Rating System (HERS) rater will conduct an energy audit on your property to project the estimated savings, ensuring the upgrades are financially beneficial.

Q5: Why should I get a second opinion on my energy-efficient mortgage?

Lenders offer varying rates and fees. As experts at providing second opinions on energy-efficient mortgages, Sauk Mortgage Group can review your current offer to potentially save you thousands over the life of your loan.

Related Posts