What is a HELOC and How Does It Work? If you are a homeowner in…

Cash-Out Refinancing in 2026: How Columbus Homeowners Can Tap Equity for Renovations, Debt Consolidation, or Family Goals

Why 2026 is a Prime Time for a Cash-Out Refinance in Central Ohio

The Columbus real estate market has seen incredible growth over the past few years, leaving many homeowners sitting on a substantial amount of untapped home equity. As we navigate 2026, a cash-out refinance remains one of the most powerful financial tools available to Central Ohio residents.

A cash-out refinance replaces your current mortgage with a new, larger loan, allowing you to pocket the difference in cash. Whether you live in Dublin, Westerville, or right in the heart of Columbus, leveraging this equity can help you achieve major financial milestones without relying on high-interest credit cards or personal loans.

- Fund Home Renovations: Upgrade your kitchen or add a home office to increase your property value.

- Consolidate Debt: Pay off high-interest debts to improve your monthly cash flow.

- Support Family Goals: Cover college tuition or help a child with their first home down payment.

Working with a local expert like Sauk Mortgage Group ensures you get a loan structured specifically for your unique situation.

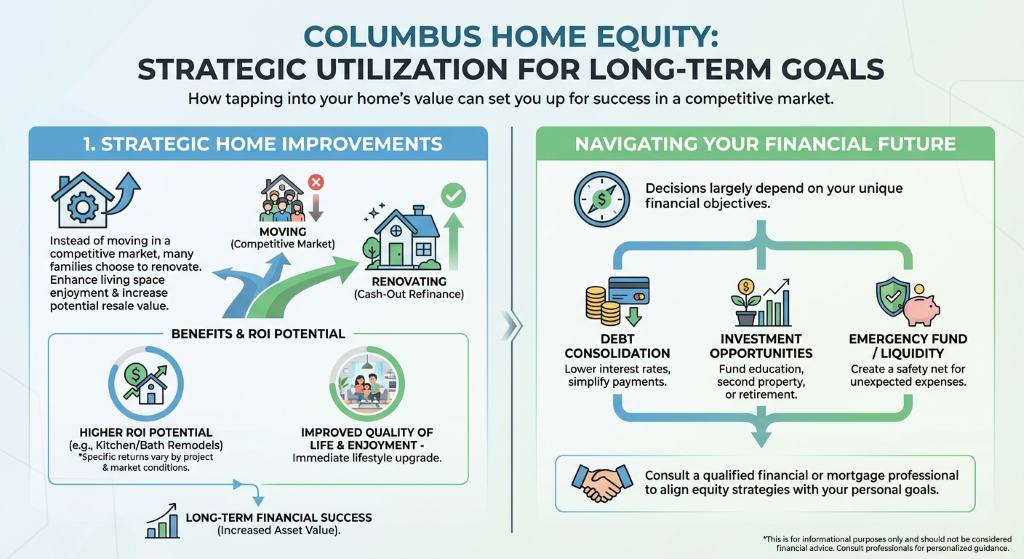

Top Ways to Use Your Home Equity in 2026

Many Columbus homeowners are asking how they can best utilize their equity this year. The answer largely depends on your long-term financial goals. Here is a closer look at how tapping into your home’s value can set you up for success.

1. Strategic Home Improvements

Instead of moving in a competitive market, many families choose to renovate. Using a cash-out refinance for home improvements not only makes your living space more enjoyable but can also yield a high return on investment when it is time to sell.

2. Smart Debt Consolidation

With credit card interest rates fluctuating, consolidating debt into a single, lower-interest mortgage payment is a savvy move. This strategy can significantly lower your monthly expenses and simplify your financial life.

3. Investing in Family Milestones

From funding higher education to purchasing an investment property in Ohio, the cash from your home equity can provide the upfront capital needed for major life events. As a dedicated mortgage broker, Joseph Sauk helps you crunch the numbers to ensure this strategy aligns with your financial future.

| Financing Method | Estimated Interest Rate (2026) | Typical Repayment Term | Best Use Case |

|---|---|---|---|

| Cash-Out Refinance | 6.0% – 7.5% | 15 to 30 Years | Large renovations, major debt consolidation |

| Credit Cards | 20% – 24% | Revolving | Small, short-term purchases |

| Personal Loans | 10% – 15% | 3 to 7 Years | Mid-sized expenses, quick funding |

| HELOC | 8.0% – 10.0% | 10-Year Draw Period | Ongoing projects with variable costs |

The Benefits of Working with an Experienced Columbus Mortgage Broker

Navigating the mortgage landscape in 2026 requires local expertise. When you partner with Sauk Mortgage Group, you are not just getting a loan; you are gaining a financial advisor who understands the Columbus market inside and out.

Unlike large retail banks that offer a one-size-fits-all product, an independent mortgage broker shops around on your behalf. We compare rates from multiple lenders to find the most competitive terms for your cash-out refinance. Furthermore, we handle the complex paperwork and communicate with you every step of the way, ensuring a smooth and stress-free closing process.

Whether your goal is to remodel your kitchen, eliminate high-interest debt, or secure funds for a family investment, having a seasoned professional in your corner makes all the difference.

Q1: What are the requirements for a cash-out refinance in Ohio?

Generally, you need a credit score of at least 620, a debt-to-income ratio below 45 percent, and enough home equity to leave 20 percent in the home after the refinance.

Q2: How long does the cash-out refinance process take in Columbus?

The process typically takes between 30 and 45 days, depending on how quickly the appraisal is completed and how fast you provide the required documentation.

Q3: Is the cash I receive from refinancing considered taxable income?

No, the funds you receive from a cash-out refinance are considered a loan, not income, so they are not subject to income tax.

Q4: Can I use the cash to buy a second home or investment property?

Absolutely. Many homeowners leverage their primary residence’s equity to secure a down payment for an investment property or a vacation home.

Q5: Does a cash-out refinance restart my mortgage term?

Yes, because it is a brand new loan. However, you can choose a shorter term, such as a 15-year mortgage, if you want to pay it off faster.

Related Posts